What are Target Retirement funds?

Co-Authored and Reviewed by Gagan Sandhu, MBA - The University of Chicago Booth School of Business, CEO of Xillion

Posted on . 4 min read

If you’ve invested in a 401k or other tax-benefit retirement account, chances are, you’ve come across a target date retirement account. Examples include “Vanguard Target Retirement 2050 Fund” or “Fidelity Freedom 2045 Fund.” While these funds are convenient, there are a few reasons why you might want to stay away from them.

But what exactly are these funds? Target retirement funds are supposed to further simplify retirement investing by automatically shifting your allocation of investment assets - between stocks, bonds, and treasuries - as you get closer to retirement.

For example, a retirement fund might start out with a higher percentage of stocks when you are younger and have a longer investment time horizon before retirement. As you get closer to retirement, the allocation might shift to a higher percentage of bonds, which are generally considered to be less risky.

In general, your investment portfolio should carry less risk as you get closer to retirement. You can usually afford to be invested in equities when you’re younger, since you have a long time horizon to stay in the market. Over the past 30 years, the S&P 500 has provided a predictable return of around 11% per year. But when you retire, you rely on your investment savings to live. It’s not worth the risk that the equities markets go so low that you can’t afford to live.

In recent years, target funds have become a big business. Morningstar compiled the following data on target funds:

-

Assets in target date funds stood at $3.3 trillion in 2021, up from $2.8 trillion in 2020.

-

Vanguard had the most money in target retirement funds, with more than $55 billion in investment inflows in 2021.

-

Fidelity, T Rowe Price, and Blackrock took the next-largest slice of market share, with 14%, 11.5%, and 8.8% of estimated share, respectively.

Target funds might sound like a great option. In some cases, they can be. But there are a few drawbacks:

-

High Fees. The average target fund had an asset-weighted fee of 0.34% in 2021, according to Morningstar. That is much higher than the fees you would pay by managing the money yourself. With Vanguard’s S&P 500 fund, for example, you only pay a fee of 0.03% — less than one-tenth the target fund fee! That’s a heavy price to pay for convenience.

-

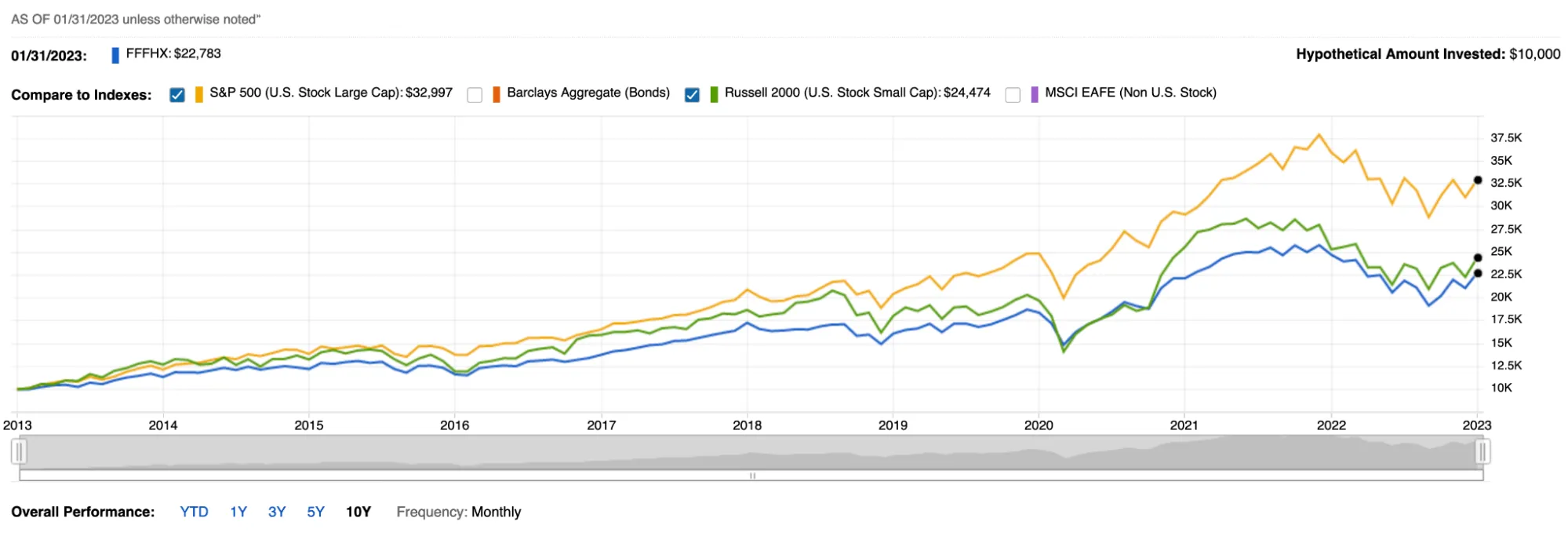

Too Conservative. For younger people, target date funds can often be too risk averse. Most people under 35 years of age are better off investing in low cost S&P 500 or Russell 2000 index funds and not worrying about anything else until they are closer to 50 years old. Then you can rebalance your portfolio by spending only a few minutes every quarter. Here are the 10 year returns of target funds vs S&P 500 and Russell 2000:

- Lack of Customizability. Everyone has their own journey toward financial independence. It’s important to optimize your path. That might mean investing in individual equities, in specialized index funds, or even angel investing. Target funds simply don’t give you the flexibility you need to optimize your retirement path. They can be useful if you aren’t willing to put the time in to customize your financial path — but by taking even a few minutes every month, you can forge a better path to financial freedom.

More on target date funds.

Convenient? Yes. Optimal? Definitely not.

Xillion gives you the best of both worlds: convenience and optimization.

It only takes a few minutes to shift your funds from a high-fee target funds to your own mix of index funds and other investment types.

📉 Your 401k plans default to target date funds.

📈 But you can do much better by investing directly in low cost index funds like FXAIX, VOO, VUG etc. Why?

1️⃣ Target date funds have much higher fees (10x more) than the cheapest index funds.

2️⃣ Target funds are too conservative, especially for people under 40 years of age (see graph).

3️⃣ You can't customize your investments the way want.

Xillion can help. The convenience of target funds might be tempting. But Xillion can take a lot of the hassle out of forging your own financial path. For example, we’ll scan your portfolio to look for funds that have unnecessarily high management fees. We can also help you plan for retirement, mixing assets in a way that aligns with your financial goals. Get started today with a free Xillion account!