The Fed wants to eliminate jobs, whether they admit it or not

Co-Authored and Reviewed by Gagan Sandhu, MBA - The University of Chicago Booth School of Business, CEO of Xillion

Posted on . 4 min read

The Federal Reserve has two primary duties: promote price stability (tame inflation) and keep unemployment low. Unfortunately, those two goals often directly conflict with one another. When labor demand is low, companies can attract workers with lower wages, so the price of goods and services goes down. On the other hand, high employment means workers can bargain for higher wages, thus increasing the cost of goods and services.

The Fed has been raising interest rates at a historic pace since March 2022. The official reason is to lower inflation to a 2% goal, which is true but not the whole story. To get 2% inflation, the Fed wants (and perhaps needs) to raise unemployment. Officially, they call this an "unintended consequence," but that's a pretty pathetic excuse. It's like saying a dead cow is an "unintended consequence" of hamburgers. Or that death is an "unintended consequence" of war. In other words, it may be "unintended," but it is also a direct and predictable consequence --- one that you choose to accept if you embark on a certain endeavor.

Fed Chairman Jerome Powell understandably avoids framing the interest rate hike in terms of unemployment. In a heated exchange with Senator Elizabeth Warren, Powell said "We actually don't think that we need to see a sharp or enormous increase in unemployment to get inflation under control." Warren responded by pointing to the Fed's own projections, which propose rate hikes that would lead to 2 million lost jobs. Warren also noted that, in 11 or the last 12 times that the U.S. unemployment rate went up by at least one percentage point, it then went up by another percentage point within the year. The Massachusetts Senator likened "planned" unemployment to a runaway train that's difficult to control once it gets started.

Powell is likely obscuring the Fed's intention to raise unemployment. This makes sense, as the optics would be horrible, especially after the Fed stepped in to limit the losses of relatively wealthy Silicon Valley Bank depositors. But the Federal Reserve needed to do something to curb inflation. And interest rate hikes hurt everyone, even if the working and middle-class bear the brunt of it. When the Federal Reserve was created after the Panic of 1907, the Wilson administration intentionally insulated it from political pressure because they knew the Fed would need to make difficult and unpopular decisions, just as it's doing now.

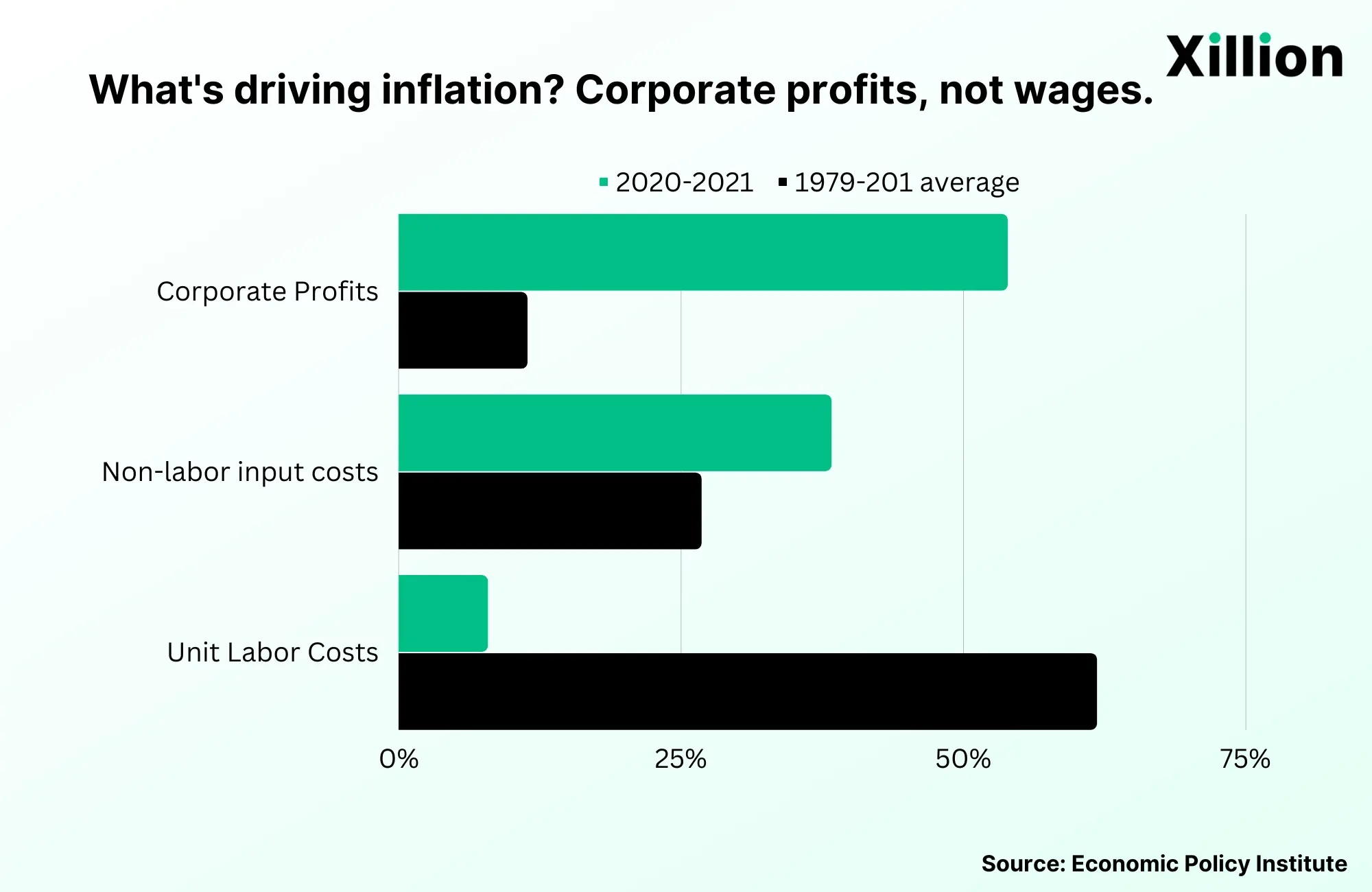

One weird thing that doesn't get mentioned in this story: Wage inflation isn't even driving that much of the current inflation. Employers frequently gripe about how difficult it has been to hire people right now. While wages modestly increased after COVID, real wages (those adjusted for inflation) actually decreased since 2021. In fact, according to an analysis from the Economic Policy Institute, labor costs only accounted for 7.9% of price inflation, compared to 53.9% from corporate profits and 38.3% from nonlabor input costs. Those other costs include rising energy prices resulting from the Ukraine war and Russian sanctions.

At least for now, despite all the scary headlines, the economy is doing quite well. In fact, the March unemployment rate stood at only 3.6% in the U.S. Wages have been cooling since the end of 2021, especially in the leisure and hospitality sector, which struggled to attract enough workers post-COVID.

What does this mean for your job security?

Many of Xillion's customers are knowledge workers in tech and business. Those sectors have actually been hit harder and earlier than lower-wage jobs. If the Fed can tame inflation without causing much more damage, you may be in the clear. The Fed is playing with fire, but so far it has managed not to get burned --- unemployment is still low, and inflation is going down.

It all depends on how much more they want to raise rates. If the Fed actually wants to get inflation down to 2%, then interest rate hikes will need to continue for at least a few more months. According to the Fed's own projections, the U.S. can reach 3.3% inflation by the end of 2023 and 2.5% by 2024.

The resultant economic pain might also be backloaded, especially since several of the drivers of inflation are not due to fiscal policy but broader real-world supply chain issues. Some economists have suggested the Fed should revise its inflation target to 3% as a compromise. Powell has rejected this suggestion.

Source: New York Times

What does this mean for my portfolio?

If you were only looking at Finance Twitter, you'd think we were already in the Great Depression. But overall, the stock market is doing well, and from mid-October until today, the S&P 500 has rallied 15%. We are still about 15% below the all-time high reached at the end of 2021.

In recent months, tech stocks have been the primary driver of the market rally. Advancements in AI also represent a potential exogenous factor that could boost employment in the industry, even if the Fed policy works against it.

The "soft landing" is still possible, but it's difficult to predict what will happen with the broader economy. We can only hope Powell manages to keep the "unintended consequences" under control.