Beyond Interest Rates: Exploring Tax Benefits, Rent Costs, Appreciation, and More in Your Housing Decision

Co-Authored and Reviewed by Gagan Sandhu, MBA - The University of Chicago Booth School of Business, CEO of Xillion

Posted on . 2 min read

If you pay attention to the financial news, you’ve undoubtedly heard about 7% mortgage rates. The memes would have you believe the lucky few who purchased homes with 3% mortgage rates are living like kings, while the rest of us missed our golden opportunity and will be renting forever. After all, the price of housing is supposed to go down when mortgage rates go up, but the U.S. housing market is still red-hot even after the rate hikes.

The truth is more complicated. While mortgage rates make a significant impact on how much you pay for a home, it might not necessarily be as large as you expect. For example, if you pay a 20% down payment on a $440,000 with 7% interest rate, you would pay a monthly payment of $2,300. WIth a 6% interest rate, your payment would be $2,100.

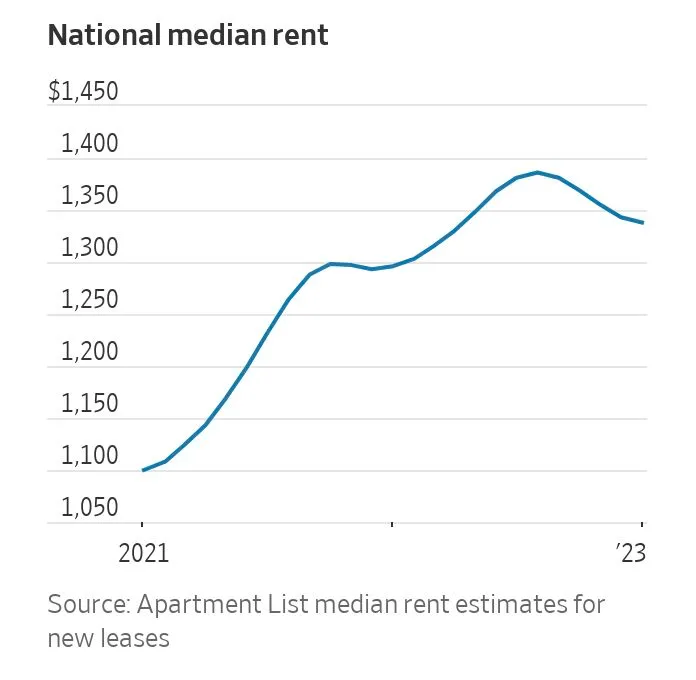

Both of those figures might sound too high, but it’s important to compare that monthly figure with the cost of renting. Also factor in other cost sources, such as local income tax, maintenance, and upkeep. Expected appreciation or depreciation should also go into your home-buying decision. One big difference between renting and owning? A mortgage locks in your monthly payment price, while renting fluctuates every time you renew.

Many people don’t take the time to make that calculation, which is by far the most important one you can make in your home-buying journey. That’s exactly why we created the Xillion Mortgage Calculator — it takes everything into account, and lets you know whether you should rent or buy a new home.

According to our research, the majority of renters do not take the time to compare the expected cost of renting versus buying a home. Oftentimes, these buyers simply rely on gloomy news headlines to decide they’ll never be able to afford a home — which often isn’t true.

It’s easy to also get stuck in a pattern of wishful thinking. Instead of thinking about whether you should have purchased a house five years ago, focus on the decision today. Of course it would have been better to purchase with lower interest rates. But there is no point in dwelling in the past. And in fact, you can still reap considerable upside by making the right decision today.

So don’t delay more. Go to Xillion and use our Xillion Mortgage Calculator to make the optimal housing decision. You will reach your financial goals sooner, with the peace of mind of knowing you made the right call.