Emergency Savings Guide

Posted on . 4 min read

In the tech sector alone, more than 100,000 people have lost their jobs in the last few months. Companies ranging from Microsoft, Tesla, Netflix, Robinhood, Coinbase, Shopify, Redfin, Peloton, Carvana, JP Morgan etc have been laying off employees by hundreds if not thousands. We are either already in a recession or slowly sliding into one.

Although there’s no ideal way to predict & prepare for all future events, taking a few simple steps is likely to reduce stress for your family during these uncertain times. Without preparation, a panic is likely to set in, which could lead to suboptimal decisions. To prepare for the slightly uncertain future:

a) Set up an emergency fund.

b) Tighten your belt a little bit by cutting some unnecessary expenses.

c) Do not panic sell all your stock investments.

d) Invest some of the extra savings (if stashed away) into growth stocks that are selling at a huge discount right now.

We'll cover all these topics over the next few weeks, but today in this blog, let’s discuss how much money to put into an emergency fund so that you have enough to weather any possible storm but not so much that you could be losing money by letting it sit idle.

What’s an Emergency Fund?

An emergency savings fund comes in clutch in case of urgent matters such as your car suddenly breaking down and you needing to buy a new one immediately. Or an urgent travel plan to visit family or friends. Or a surprise dental surgery. Or to pay for a health emergency if you have a high deductible plan.

The Basics

Let’s keep it simple. If you have insurance coverage for health, life, home and auto, the emergency funds only need to cover expenses for a few months (if you don’t have all of the insurance coverage listed, please stop reading this and first get those). But how many months, you might ask? Great question!

Although it’s a matter of personal choice, a little bit of math and economics can make this decision a whole lot easier. Let’s dive in.

How to Calculate

Even though some old school finance talking heads would tell you that everyone needs 6-12 months of expenses in their savings account, we are going to be much more methodical in giving you a number that is most suitable for you. Here are some factors to consider when planning your emergency savings fund:

| Need a bit less if... | Need a bit more if... | |

|---|---|---|

| Job Stability? | Your job is stable. Nurses, doctors, dentists, teachers, federal/state/county workers etc. | Your job is a bit unstable (e.g. tech workers) or you have a seasonal job. |

| Working Spouse? | Your spouse is also earning. | You are a single income household, which invariably means a little more concentrated risk. |

| Employer Pays Severance? | Your employer pays severance, which can cover expenses for a few months. | No severance payment is guaranteed. Or severance would be minimal or delayed by a few weeks. |

| Have Liquid Assets (stocks etc)? | You have stocks, bonds etc because they can act as emergency ATMs where you can borrow against them fairly easily (we recommend never borrowing more than 20% of the total value). | You don’t own stocks, bonds etc but rather have your money invested in real estate, whether residential or commercial. |

| Easy Access to Loans? | You can easily tap into a home equity line of credit (HELOC) in case of emergencies.In general, getting a HELOC is almost always a good idea. | You don’t believe in taking debt to pay for emergencies. Or if you don’t own real estate. |

| Your Risk Appetite | You like to live on the edge! Or at least you are a bit more comfortable with the uncertainty that the future might bring. | You prioritize sleeping peacefully and never worrying about any unforeseen circumstances. |

There are a few other factors such as unemployment insurance, family support etc that can play a smaller role, but the factors listed above cover a big chunk of the variables.

Help is on the way!

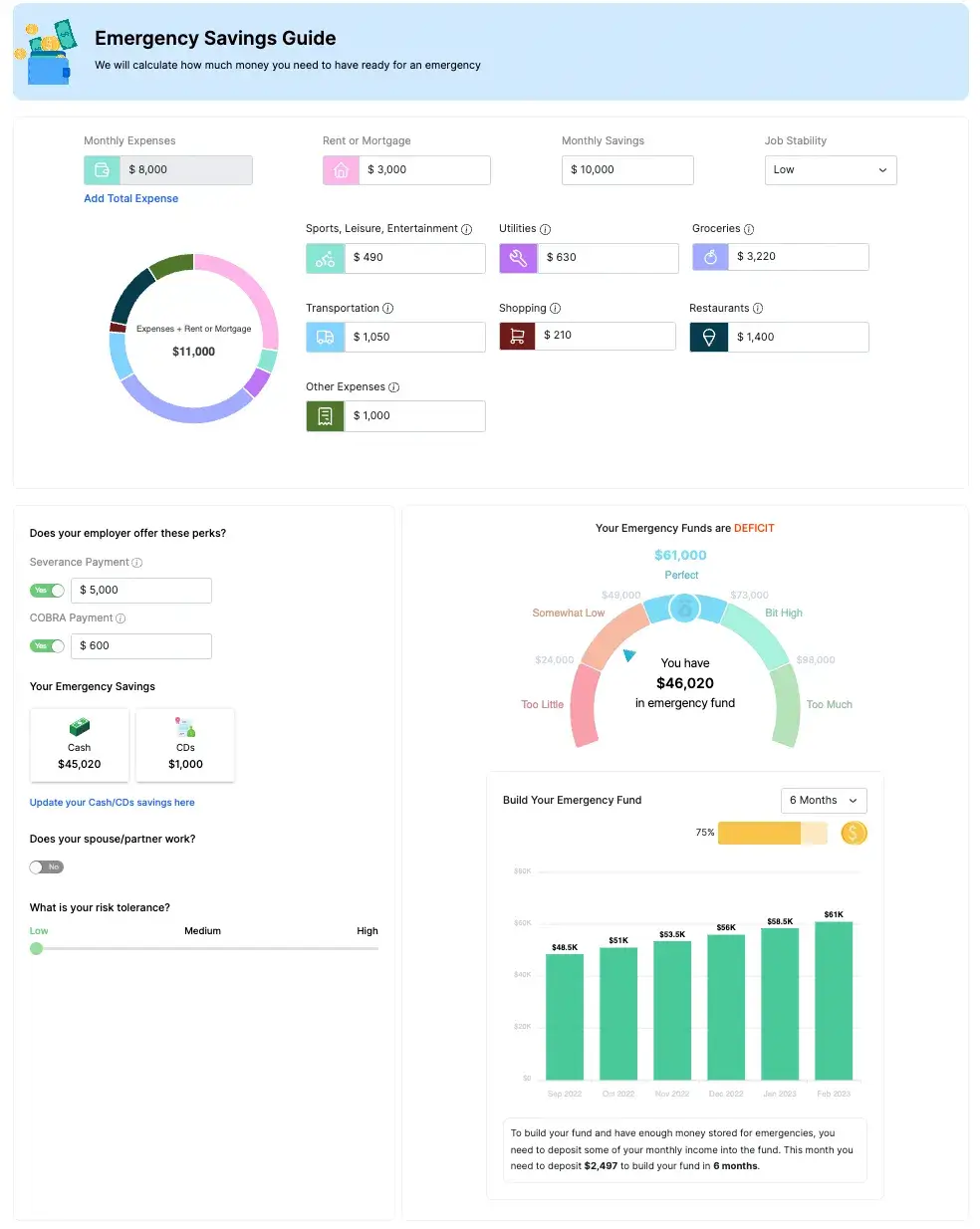

But all that is a lot to consider when making financial decisions. Rest easy! We have added all these factors, and much more, and created a nifty tool that gives you an answer in less than 2 minutes about how much money to save. Try it yourself at Xillion - Emergency Savings Guide.

In addition to helping you calculate the savings amount and create a plan to reach this goal, we also suggest what to do if you have excess savings. Hint: invest excess savings into growth stocks and index funds. We also help you see how your excess savings will grow in the future.

PS: Here’s a fun fact. More Xillion customers had too much money saved up for emergencies than too little. Many of the customers we spoke with had in excess of $100,000 sitting in their savings accounts! Xillion helped them invest this money wisely so it could grow, rather than get wasted away by inflation in a savings account.